RELATED LINKS

RELATED LINKS

I WANT

RELATES LINKS

RELATES LINKS

Services

Related Links

Use and Management of Cookies

We use cookies and other similar technologies on our website to enhance your browsing experience. For more information, please visit our Cookies Notice.

- Personal Banking

- Stories & Tips

- Tips for You

- Explore the symptoms of debtor

- Personal Banking

- ...

- Explore the symptoms of debtor

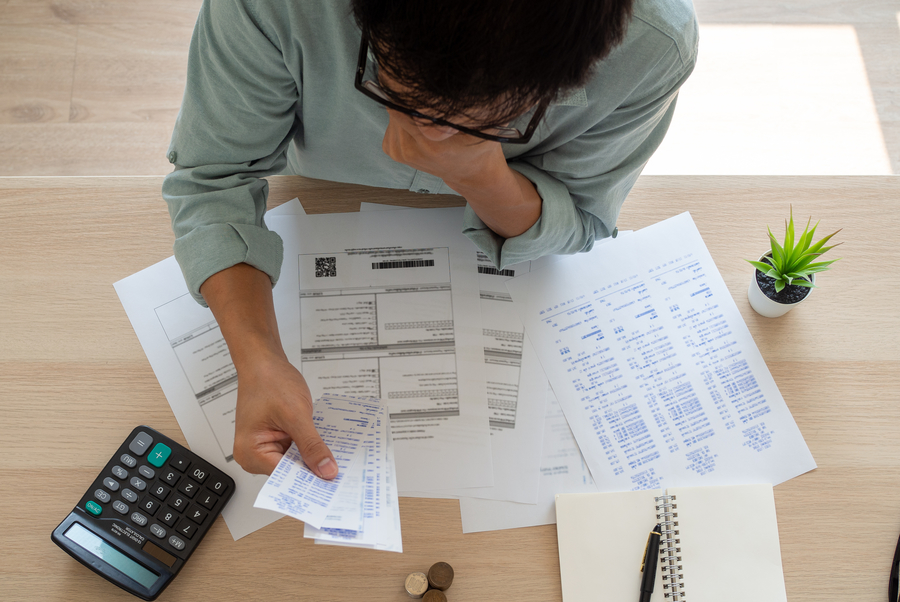

Explore the symptoms of debtor

20-04-2020

You may still remember the former No.1 tennis player in the world who was decided by the court to put off his trophy to auction in London in order to pay for the debt of more than US$ 80 million or approximately Baht 2,500 million he committed.

Ever since he quit playing tennis, the income of about US$ 130 million he had collected was fully spent. He also borrowed more money and was unable to pay back. Finally, the court decided that he was bankrupt for the reason of being "failed to pay the debt".

In 2009, Sports Illustrated magazine revealed the numbers about the financial problems of professional athletes. It was found that about 60% of basketball players broke within 5 years after stop playing while American football players had a bankruptcy rate of nearly 80% within the first 2 years of quitting their occupation.

Let’s see the UK side. A charity named Xpro revealed information in 2013 that 3 out of 5 Premier League footballers became bankrupt within 5 years after retiring. There is a doubt of why there is a high bankruptcy rate when the leading professional athletes, who make a lot of money in various sports such as Premier League footballers make US$ 3.3 million per year, or about Baht 102 million per year, quit their job.

The answer is overspending, ignoring to save money and having not good financial discipline. Regardless of how much income you earn, if you don’t have financial discipline, there will be a high chance that you will become insolvent. When that day comes, you need to find a way out with a loan. And if you cannot pay back in time, the debt will increase steadily. Finally, you become a person with insolvent debt.

Therefore, you should think carefully before loan, survey yourself whether you are able to pay back. In principle, each person’s total debt should not exceed 1 in 3 of monthly income.

For example, with a salary of 20,000 baht, the monthly debt burden should not exceed 6,666 baht (20,000 divided by 3 equals 6,666 baht). This means that after dividing the money to pay the debt, there is still a surplus including saving money. On the contrary, if you have a debt burden of more than 6,666 baht, it may be a warning sign that the monthly debt burden is too high.

There is probably no problem for those who can pay the debt. But for those with high debt, they are often unhappy and usually show their personal symptoms as follows;

1. Restless

The burden of debt is overwhelming due to self. And even when it's time to pay the debt and not getting the money in time, the symptoms tend to be unhappy, being restless, anxious, whatever eaten is not good, sleepless, think all the time where to find the money for creditor.

2. Do not like talking about money

When people talk about money matters, they don't want to get involved with the conversation because it seems to nudge the scar in their hearts. If having a lot of debt, they might be shocked when hearing people talking about money..You may notice that people having much debt like to keep themselves alone.

3. Late payment arises

These are the warning signs that the debt becomes too high e.g. late payment happens, unable to pay the full amount, withdraw saving money to pay for debts.

4. The debit balance does not reduce

Normally, when paying off debt, its balance will gradually decrease. But if the balance is found increased, this shows that new debt has been created which causes the increase of principal and interest burden.

When you check yourself and find that you get one of the above symptoms, firstly just calm down and don't escape from the problem, then take action to fix.

1. To do Expenses list and cut the unnecessary expenses off

The easy way is to write down all monthly expenses and do list all unnecessary expenses such as movies, dining out, monthly gym fees, and various extravagant expenses. Then promise yourself that you will no longer buy unnecessary items, it will be more economical and frugal.

2. Prioritize debt payment

Write down all debts and rank them with the highest interest first. And gradually level down per rate of interest. Then clear all high-interest debt first, such as informal debt, cash card debt. Credit card debt

3. Stop creating new debt.

The way to control the debt burden be not higher than is to stop creating new debt. You must have a commitment to yourself that you will not create a new debt until the existing one is cleared.

4. Sell some assets to pay off debts

Even though you have extremely been economical, the debt burden has decreased slightly. If this is the case, you might have to explore what assets you have in order to sell them out and pay off the debt. Sometimes assets that even have psychological value but you have to cut off in exchange for happiness in the long-term

5. Consolidate debt

Another solution for a debt problems is debt consolidation, but it is most successful with a very low amounts, i.e. one hundred thousand baht and with the same type of debt, such as debt from 5 credit cards. The method is to combine all existing credit card debt to be one unit in order to reduce the interest burden from all credit cards, to pay only one interest rate.

In this way, the debtor needs to negotiate with the credit card issuer. (Financial institution) how to consolidate debt including the type of refinancing credit card debt, e.g. requesting of personal loans which the borrower can request of up to 5 times the income amount with low interest (Lower than interest on credit cards). Next, take a new loan to pay off credit card debt.

Having debt is definitely unhappy life. Anyone who has experience would know very well about the suffering from debt. So, if you do not want to live with debt for a lifetime, a simple solution is to have financial discipline, know how to keep, know how to use it. If you can, life will be debt-free and happy.